The Future of RTX...

Analyzing RTX's reorganization (merger, divestitures, rebranding) plan

Summary:

RTX key events within last 3 years

Brief analysis of RTX Q2 2022 reorganization plans

Qualitative analysis of RTX’s recent divestitures

Future prediction of RTX’s asset portfolio

In the last article, I presented a long investment pitch for Raytheon Technologies (RTX). It turned out to be somewhat correct as the couple days following when the Q3 earnings report came out, the stock price rose ~10% since the time of when my article came out. I thought RTX was super interesting so decided to continue to write about its newest development which is the sale of Raytheon’s Cyber and Intelligence business for $1.3 billion. This later prompted me to do more research on its past mergers, acquisitions, and divestitures, and ultimately what it means for the future of RTX.

Recent RTX Key events

Let’s first start during peak COVID era on April 3, 2020, when Raytheon Company announced the completion of an all-stock merger of equals with United Technologies Corporation to form Raytheon Technologies. For some background, Raythoeon was strictly a defense systems company while United Technology was a conglomerate in the aerospace, defense, and industrials industries. A couple of months before the merger, United Technologies sold off its industrial businesses: Otis Elevator Company, manufacturers of elevators, escalators and walkways; and Carrier business which was a global manufacturer of HVAC systems.

After the merger, Raytheon Technologies reorganized to be made up of 4 segments: Raytheon Intelligence & Space (RIS), Raytheon Missile & Defense (RMD), Collins Aerospace, and Pratt & Whitney, with the latter 2 segments originating from United Technologies.

Since then, there has been significant reorganization and portfolio transformation within Raytheon Technologies. In Q4 2021, Raytheon announced the divestiture of its defense training and logistics business for $1.5 billion. In Q2 2023, Raytheon announced the sale of Collin’s actuation business for $1.8 billion in cash. Only weeks after, Raytheon announced a consolidation of its RIS and RMD segments to form Raytheon under a new name RTX. As part of this realignment, Collins Aerospace absorbed the Command and Control, and Air Traffic Management division which was previously under RIS. RTX also moved Collins's Aerospace Intelligence, Surveillance and Reconnaissance business to the Raytheon segment. And lastly, BBN Technologies moving from RIS to RTX corporate

Now most recently, in Q3 of this year, RTX is planning to sell Raytheon’s cyber services division for $1.3 billion in cash.

What was the reasoning behind the reorganization strategy?

First, let's focus on the reason behind RTX’s reorganization in Q2 2023. In this reorganization process, Raytheon Technologies started trading under RTX, while RIS and RMD divisions consolidated to form the Raytheon segment along with Pratt & Whitney, and Collins Aerospace as the other 2 segments. There was also significant realignment of divisions which drastically changed the focus of each segment. The most obvious reason behind this change was to realign and reduce manufacturing costs. Before the reorganization, there was significant overlap in the type of industries and clients. The Collins Aerospace segment product clients mainly focused on products related to aviation systems across the aerospace and commercial industries. The Pratt & Whitney segment focused on aviation engines for both commercial and military clients. Lasty, RMD and RIS focused solely on military products.

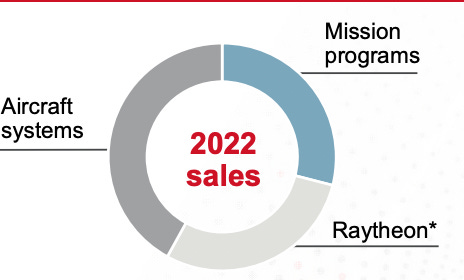

The reorganization allowed Collins Aerospace and Raytheon to realign its product lines to best fit its manufacturing capabilities and target clients. Currently, Collins Aerospace’s portfolio is representative of almost ⅓ of Raytheon's businesses. This can be attributed to Collins Aerospace taking over Raytheon's Command and Control, and Air Traffic Management division. This decision makes sense as the products within this division are more aligned with the commercial space rather than the defense space. Additionally the Intelligence, Surveillance, and Reconnaissance business more aligns with Raytheon's defense service business.

Collin’s Aerospace new portfolio in sales (Sourced from Investor Day Presentation)

The operational strategy behind the 2 divestitures

After the merger with United Technologies, RTX executives continued to stress the importance of constant readjustment of its portfolio. One of those solutions, besides the reorganization of its segments, is divestitures of assets and/or divisions. In this section, we will analyze RTX’s divestment of Collins Actuation and Flight control systems, as well as Raytheon’s cyber business.

To provide some context, Raytheon also sold its global training and logistics business in 2021, which accumulated almost $1 billion in sales. In the 2021 investor day, Greg Hayes, CEO of RTX, said the business “is not a bad business, but not a growth business” and that at the time this was “really just the beginning” of its transformation. This is important to keep in mind as we analyze Haye’s decision in their most recent divestitures. It is clear Haye wants to remove the cost-inefficient businesses while maintaining focus on its core growth businesses.

From an overarching view, these most recent divestments will bring in $3 million in cash which will support RTX’s new $10 billion share repurchase program initiative. However, there are more questions that need to be answered such as were these divestments even correct/necessary? What were the other supporting reasons for RTX to make this decision? After understanding all of this, can we make a reasonable assumption of RTX’s portfolio strategy for the future?

Divestment of Collins Aerospace Actuation and Flight control systems business

On July 21, 2023, Collins Aerospace Actuation and Flight control systems for $1.8 billion in cash to Safran Group. According to Safran’s press release, the business is expected to generate $130 million in EBITDA and $1.5 billion in sales for 2024E. For RTX, this is representative of 1.5-2% of RTX’s total sales and 5-7% of Collins Aerospace's sales. Although not a huge loss to Collins Aerospace or RTX, let's still investigate why this divestment occurred.

The most obvious reason is that this is not a high-performing business or even loss incurring business. Additionally, the industry itself has a high barrier to entry which could have resulted in RTX's inability or loss of interest to continue. This is because the products and systems are particularly difficult to manufacture and most systems are built to the client’s specifications. Thus, a specific and intricate manufacturing focus might have deterred RTX. Moreover, RTX is based in the U.S. while 7/8 of the manufacturing locations for this business are based in Europe, making it difficult for RTX to remain operationally focused on this business given the long distance.

Additionally, Safran CEO Olivier Andries states that “maintenance accounts for over 40% of revenues”. For a business focused in this industry, this is 100% a tailwind. However, if you are not, such as RTX, there is a good chance that resources are not being used to keep up with these accounts as they are highly complex and most likely cost-intensive. This is also indicative of a sticky customer base, which RTX may have found it difficult to acquire a larger market share. Therefore, if we sum all the pieces together, it would be safe to assume that because it is a difficult industry to succeed in, and it is not a high growth or high margin portion of the business, there is no marginal benefit for this RTX to keep this business around.

Divestment of Raytheon’s Cyber, Intelligence and Services business

The divestment of Raytheon’s Cyber business for $1.3 billion in cash to an unknown party is far more straightforward in identifying the plausible reasons. The primary catalyst for this divestment is that the cash proceeds from this divestment will support the $10 billion share repurchase program, in addition to the proceeds from the Collins aerospace actuation business divestment.

However additional factors could have been that this business is not financially stable or even growing enough where it could be considered essential for its future strategy. The Raytheon segment itself has historically focused on defense products rather than defense software/services. It was not only until 2010, that Raytheon acquired a cyber solutions provider. Additionally, two more acquisitions in this defense software space continued in 2014 and 2015. In the future, it seems that Raytheon is straying away from the defense SaaS business.

Additionally, this can be attributed to the type of business model which the Cyber business relies on. First, Raytheon as a whole receives defense contracts from national militaries such as the U.S. military. In addition, many of the contracts that the Cyber business receives are large one-time contracts to build out cyber security software. For example, in 2018 the U.S. Department of Homeland and Security (DHS) awarded the DOMino contract to Raytheon for $1 billion dollars over 5 years, to support the development of DHS's next-generation national cybersecurity protection system. As shown above, these revenue streams are extremely lumpy as one or two contracts can make up a majority of the business’s revenue. At the same time, there are inherently high R&D and operational costs associated with these contracts as they are most likely built to client specifications. Therefore, in the eyes of executives, this business is not essential and could inhibit the resources required for its core strategy of defense weaponry.

What's next?

I would not be surprised if Raytheon’s Space business is the next one to go, especially if Raytheon starts to incur further losses from its manufacturing issues, or if more cash is required. Similarly, to its Cyber business, the Space business model is extremely unpredictable and is definitely not considered essential to RTX. There has been no information about any backlog related to its space business which points to the fact that it is not a high-growth business. Since the business was founded pre-merger, and there now seems to be a focus on commercial aerospace, it does not seem likely RTX views this business as part of its post-merger initiatives.